| Hi - here are your latest deals, freebies, tricks and messages to help you save.  THE TOP TIPS IN THIS EMAIL

| | Warning: Only 3mths left to reclaim PPI

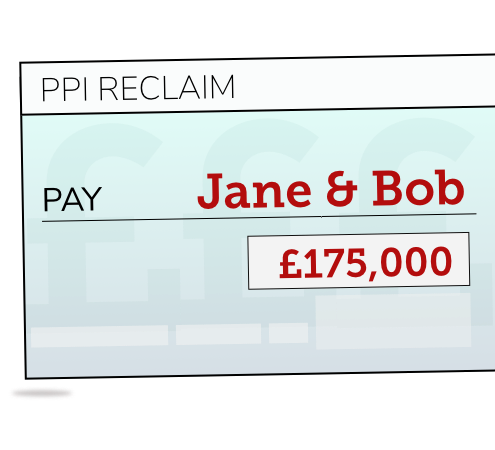

Today we reveal the biggest PPI payout we've seen - a life-changing £175,000 Use it as inspiration to check if you're owed £1,000s - and we show how to do it for FREE and beat the deadline A jaw-dropping £34.4 billion has already been paid to millions who were mis-sold PPI - but hundreds of millions of pounds is still to be repaid. While we've screamed about how to reclaim for years, now our clarion call has added urgency ahead of the 29 Aug deadline. So check NOW if you're owed via our Free PPI reclaim tool and guide.  To spur you on, a retired MoneySaving couple from Swindon today tell their story of how they've cleared their mortgage and have become debt-free after reclaiming a remarkable £175,000 on various credit cards and a loan going back 20yrs. To spur you on, a retired MoneySaving couple from Swindon today tell their story of how they've cleared their mortgage and have become debt-free after reclaiming a remarkable £175,000 on various credit cards and a loan going back 20yrs. Jane says: "We originally thought about applying but didn't. Then we read all the information on MSE and gave it a go. The banks made it difficult but we kept on going and succeeded. "Getting this money has given us peace of mind as we can look forward to retirement debt-free." For more, see Jane and Bob's incredible £175,000 PPI reclaim. Typical payouts are unsurprisingly far lower, but we regularly see £1,000s returned. So if you've had a loan, credit card, mortgage, overdraft, catalogue debt or car finance in the last 30yrs+, here's how to check if you're owed too. The bank, card firm etc must have your complaint by 11.59pm on 29 Aug or your claim won't be processed - though in reality the deadline is a little earlier that day for posted letters. If you do it by then, it doesn't matter how long the rest of the reclaim process takes - as long as you hit this deadline. Yet as you may need to do a bit of prep work, start checking if you can claim right away. And don't leave submitting your claim till the last minute anyway as it can just take the postman losing a letter or an email going astray and you're stuffed. There's nothing wrong with the concept of payment protection insurance - which covers loan, card, overdraft, mortgage and catalogue debt repayments if you can't make 'em - but banks and others massively overcharged and systemically mis-sold it for decades. This created the UK's biggest recent financial scam. There are two types of mis-selling: - Some were outright mis-sold. Banks, car salespeople, shop assistants and others may have lied that PPI was compulsory, added it without asking or failed to ensure it was suitable - see the full mis-selling checklist.

- How far back can you claim if mis-sold this way? You can go back as far as you like, though it can get harder for some if your PPI was taken out pre-2005.

- How much will you get back? If outright mis-sold, you're entitled to the full amount of PPI you paid, plus interest charged by banks on the PPI itself. Whatever that total, you get an additional 8% a year on top - a bit like savings interest - as it's assumed you'd have put that in a savings account earning interest.

- Or are you one of millions overcharged commission? Even if you wanted PPI, you were likely mis-sold due to the excessive commission taken by banks and building societies. After a landmark 2014 ruling called Plevin (the surname of the successful claimant), if more than 50% of the PPI cost included undisclosed commission (most wasn't disclosed), you're due the extra above that.

So just having had PPI means you may well have been mis-sold. Watch Martin's Plevin video to see how outrageous banks' and building societies' commission was.

- How much can I get under Plevin? It depends on the commission, but on loans, lenders typically took a HUGE 67% for themselves. On a £10k loan over 5yrs, Plevin payouts are typically £500ish.

- Can anyone claim under Plevin? No. The PPI and loan had to be active at some point since Apr 2008, though there can be exceptions. Also, you can't claim if you've already had a mis-selling payout, even if you didn't get the full sum back.

- I think I had PPI but I'm not sure I was wrongly flogged it - should I just do a Plevin claim? NO. It's VITAL to check first if you were outright mis-sold PPI as you'll get a bigger payout. If the bank rejects your mis-selling claim, it should then automatically assess you for Plevin. - First, check if you had PPI, even if you think you didn't. Scour all old credit card, mortgage, loan, store card and overdraft statements to see if there was PPI. It may also have been called 'payment insurance' or 'accident or sickness cover'.

- Can't remember the lender? All debts active in the last 6yrs are on your credit report(s) even if the accounts were opened earlier. Get your Experian report for free via the MSE Credit Club, plus see how to check other reports . It won't show whether you had PPI, just the lenders to check with.

- Not got paperwork? You can request it from your lender, and as long as the account was active in the past 6yrs the firm must keep details, regardless of when you opened it, and therefore give them to you. If it was closed more than 6yrs ago you can still ask for paperwork or whether you had PPI at all, but there's no certainty it'll have this info.

Once you've sorted your paperwork, follow the steps below...

-

Not claimed before? Do it yourself for FREE. You DON'T need to pay to reclaim - claims handlers typically take a third of your payout, often £1,000s, and do very little you can't do yourself. To do it easily, use our free reclaiming tool, powered by complaints site Resolver. It'll send your claim direct to the bank, building society etc that sold the PPI. Not claimed before? Do it yourself for FREE. You DON'T need to pay to reclaim - claims handlers typically take a third of your payout, often £1,000s, and do very little you can't do yourself. To do it easily, use our free reclaiming tool, powered by complaints site Resolver. It'll send your claim direct to the bank, building society etc that sold the PPI.

For inspiration, here's Rhoda's story: "I would like to say a big thank you for my successful overdraft PPI claim. Received £3,000 from Barclays in less than three weeks of claiming via Resolver."

- If rejected on a new claim, go to the free Financial Ombudsman Service. Sometimes when you contact banks and building societies, they say "fair cop" and pay out £1,000s in a few days.

But if they wrongly reject you (as many do) and you've exhausted their complaints processes, you've 6mths to take your case to the Financial Ombudsman Service. This independent body can adjudicate and, if it upholds your claim, force banks to pay you back.

Via our free reclaim tool you can easily escalate the case to the ombudsman if you're turned down. If you're struggling or unsure, call its helpline on 0800 121 6222.

- Even if previously rejected, many should claim again. There are 1.2m whose claims were turned down by banks, building societies and other firms (even where the ombudsman agreed with the rejection) who are now eligible again under Plevin. You should have been notified by whoever sold you PPI - if not, claim anyway.

What's more, after a ruling on commission payments in Nov, up to 150,000 previously rejected claimants should have received letters from lenders saying they can reapply.

If you got one, act on it. If you still have details from your previous claim, use those to help with your new one. However, don't worry if you don't have them as you can still try. With our free Plevin reclaim tool you only need to fill in a few straightforward details. - Payouts are normally taxed - so check if you're due this back. Most firms deduct tax automatically at the basic 20% rate on the 'savings' interest element of payouts (explained above) - not on the actual PPI you paid to the lender. While firms are only following HMRC instructions, millions could be due this money back as under the personal savings allowance - in place since April 2016 - most can now earn £1,000/yr of savings interest tax-free.

So if your payout was since then, you could be due £100s back if you needn't have paid savings tax. Read Martin's blog for info on how this works or check our guide for how to reclaim PPI tax. | | DON'T believe the fake ads on Facebook

Lots of scam ads that litter social media lie that we or Martin promote Bitcoin, binary trading etc. See Fake ads warning. | New. Shift credit/store card debt to 0% for 23mths - with NO FEE

With a balance transfer you get a new card to pay off debt on other cards, so you owe it instead, but at 0%. Do this and more of your repayments go towards clearing the debt, rather than interest. Yet there's a trade-off between the 0% length and the transfer fee, which is why a new NatWest/RBS deal is a good bet for some as there's no fee and it's a decent length - plus you get the full 23mths at 0% if accepted. W e've all the best buys below, but first, three key tips...

- Find cards most likely to accept you BEFORE you apply. Many below include a link to our Balance Transfer Eligibility Calculator. It shows your odds of being accepted before you apply, and doesn't affect your creditworthiness.

- Go for the lowest fee in the time you're sure you can repay in. If unsure, play safe and go long.

- 'Up-to' cards mean you could get a shorter 0% deal if accepted. So 'non up-to' cards offer greater certainty. New. Shift debt to 0% for 23mths with NO FEE (NatWest/RBS custs only - but with a trick for others to qualify). Sister banks NatWest and RBS last week launched the longest no-fee card - the first 0% card they've had since 2014... when they said they wouldn't be launching any more 0% cards. But to be eligible to apply you must be a current account, savings, credit card or mortgage customer of the relevant brand. Though you could just open a savings account with £1, and hey presto, you're a customer. If you don't want the faff, there are other options below (ordered by lowest fee first)... | BEST 0% NEW-CARDHOLDER BALANCE TRANSFER CARDs | | CARD + KEY INFO | 0% LENGTH (REP APR AFTER) | FEE (1) | New. NatWest (eligibility calc / apply*) or RBS ( eligibility calc / apply*) - Existing custs only (2). Longest NO-FEE 0% & you get the full 0% length if accepted.

| 23mths (19.9%) | None | | Sainsbury's Bank (apply) - Long no-fee 0%, but it's an 'up to'. | Up to 22mths (20.9%) | None | | Sainsbury's Bank (eligibility calc / apply*) - Longest 0%, but it's an 'up to'. | Up to 29mths (19.9%) | 1.5% (min £3) | | Virgin Money (eligibility calc / apply*) - Long 0% & you get the full 0% if accepted. | 28mths (21.9%) | 1.95% | | Barclaycard (apply) - Best for poorer credit scorers. | 18mths (24.9%) | 2.99% | | (1) % of debt shifted. (2) Only for existing NatWest/RBS current account, savings, credit card or mortgage customers. | Always follow the Balance Transfer Golden Rules. Full info in Best Balance Transfers (APR Examples).

a) Never miss the min monthly repayment, or you could lose the 0% deal and it'll cost far more.

b) Clear the card or balance-transfer again before the 0% ends, or the rate rockets to the higher APR.

c) Don't spend/withdraw cash. It usually isn't at the cheap rate and withdrawals hit your creditworthiness.

d) You must usually balance-transfer within 60 or 90 days to get the 0%. | New. Amazon Echo hacks, incl 99p Echo Dot or save £70+ on an Echo with a screen. It's a popular product and with plenty of tricks to cut costs (incl the short-lived 99p deal), we've rounded up 8 Amazon Echo hacks. Ditching plastic to go green? How to find 3p paper straws. With the news plastic straws will be banned in Eng next year, we've rounded up the cheapest paper, metal, bamboo etc alternatives if you want to go green right away. Reminder. Free £175 to switch to HSBC - by far the biggest upfront switch bribe. In case you missed it last week, switchers to HSBC Advance* get £175 within 40 days plus access to a 5% regular saver. To qualify, you must start a switch from your existing account within 30 days of opening (incl 2+ direct debits or standing orders), and pay in £1,750+/mth - equiv to a £26k/yr salary. You can't have had an HSBC current account since 2016. Full info and more options in Best Bank Accounts. FREE Open Farm Sunday events, incl pony rides & welly-wanging at 300+ farms. One day a year in June, they open their gates and put on activities - it's a baaaa-gain. See Open Farm Sunday for full info.

New. £40 cashback on £400 'robo-investment' (1,500 avail). If you plan to 'robo-invest' - where investments are selected by the provider based on how you answer questions on your attitude to risk - this Wealthify deal is equiv to a 9.5% head start after fees. Full explanation, plus pros and cons, in robo-investing cashback. 10,000s risk wasting up to £20,000 by repaying student loans too early. See our student loans investigation. PS: We're wishing our Coupon Kid Jordon all the best as he's back in hospital hopefully for the last time - see his blog: Coupon Kid vs Crohn's - going back under the knife for the last time (I hope). | 'I've made £1,000+ in 2019 by using my mobile' From market research to snapping job ads, here's how to turn your handset into a money-making machine Many of us are glued to our mobiles - going online, taking selfies, playing games, messaging and... er... making calls. But they can also make you cash, as many firms pay you for market research and more on them. Some dedicated users turn over a tidy sum, such as forumite Simon: "In 2019 I've made £1,060 from market research and survey apps. It required a decent effort but with minimal effort I reckon someone could still make £50/mth." We've five things to try below plus more ways to make money from your mobile, computer or tablet in 38 ways to earn cash online (plus read Simon's full story). -

New. Turn shopping receipts into cash. Don't throw away those scraps - some firms want data on consumers' shopping habits. A free app pays about £5 for every 100 receipts you upload. New. Turn shopping receipts into cash. Don't throw away those scraps - some firms want data on consumers' shopping habits. A free app pays about £5 for every 100 receipts you upload.

- Become a mobile market researcher. Some free apps pay you to snap stuff with your mobile - eg, price tags, shop layouts or even the sky (we've no idea why they can't snap the sky themselves, but hey, you're paid, so who cares). Firms offer 10p to £11 per job - some of which require a single photo, others multiple snaps.

- New. Get paid to find software bugs. Companies are desperate to make their sites and apps easier to use, so user-testing is big business. Sign up to a user-testing site, and we've seen jobs paying £20/hr. You don't officially have to be a techie, but it helps.

- Spot job ads in shop windows. Get Amazon vouchers for taking pics of vacancy signs and other job ads.

- Top 23 apps and sites that pay for your opinion. Willing to give views on pop music, politics, pasties and more? You can make cash filling in online surveys.

| Tell your friends about us They can get this email free every week | Why you should ALWAYS buy travel insurance ASAB That's As Soon As you've Booked - it doesn't cost any more to be prepared. Buy ahead and be fully protected Sun, sea, sand and sangria is around the corner for many as holidays loom, but you risk a financial catastrophe if you've paid to go away and haven't got insurance. Without it, if you need to cancel before you go - eg, you fall ill or there's a death in the family - you're not covered. Full info in Cheap Travel Insurance... in short: -

Go away twice a year or more? Annual policies usually win. They cover unlimited trips - here are the best deals: Go away twice a year or more? Annual policies usually win. They cover unlimited trips - here are the best deals:

- Just want the cheapest? These no-frills options meet our minimum cover criteria but are then based purely on price, not factoring in payout record or service. Coverwise Bronze* and Leisure Guard Lite Standard* tend to win for under-65s - eg, a 30-yr-old individual in Europe pays £9, a family worldwide £67.

- Want more cover, eg, gadgets, delays, airline failure? Use comparison sites such as MoneySupermarket*, Compare The Market*, Confused.com* and Gocompare* for more deals - then pick the cheapest of those that cover your needs.

- Want high-end protection? Our top pick is LV Premier*, based on what it covers, feedback and past payout record. It's £69 for a 30-yr-old individual in Europe, £174 for a family worldwide. Full best buys in annual policies.

- Cheapest no-frills single-trip policies from £6 in Europe, £16 worldwide. If you just want the cheapest - without factoring in payout record or customer service - Leisure Guard Lite Standard* tends to win, eg, a 30-yr-old individual in Europe pays £6 for a week (£16 worldwide), a family pays £30 for worldwide cover.

Also get quotes from MoneySupermarket*, Compare The Market*, Confused.com* and Gocompare* for a wider search or if you want to cover more - eg, gadgets, delays. See single-trip cover for more. - Over 65 or have a pre-existing condition? Don't get fleeced - here's our lowdown:

- Aged 65+? Prices can rocket, but there are competitive options from £22/yr. See Over-65s' Travel Insurance.

- Have medical issues? Always declare 'em. If getting cover's tough, see pre-existing medical conditions help.

- Travelling in Europe? Get or renew a free EHIC. It's not a substitute for insurance, but a European Health Insurance Card gives state-run hospital care in the EU at the price a local pays. If you already have one, check it's still valid as about 5 million expire annually. See How to check your EHIC & renew for free (and while we're in the EU they'll still work).

| THIS WEEK'S POLL What do you buy second-hand? It's cheap and environmentally friendly, yet some people think only new will do. Which items would you be happy to buy second-hand? Pet owners spend more on dogs than cats. In last week's poll, we asked how much you spend each year on your pet(s). More than 3,000 people responded, with 80% of dog owners spending more than £500 compared with 53% of cat owners. Other pets were more budget-friendly - a third of rabbit, guinea pig or hamster owners spend less than £100. See full pet poll results. | MARTIN'S APPEARANCES (WED 29 MAY ONWARDS) Mon 3 Jun - This Morning, ITV

Mon 3 Jun - BBC Radio 5 Live, Lunch Money Martin, noon. Listen again MSE TEAM APPEARANCES (SUBJECTS TBC) Wed 29 May - BBC Radio Cumbria, Money Talks with Ben Maeder, from 6pm

Mon 3 Jun - TalkRadio, Breakfast with Julia Hartley-Brewer, 9.45am

Mon 3 Jun - BBC Radio York, Beth McCarthy, from 7pm

Tue 4 Jun - BBC Radio Cambridgeshire, Lunchtime Live with Jeremy Sallis, 2.20pm | QUESTION OF THE WEEK Q: I'm selling my house and face an early repayment charge on my mortgage as I'm paying it off. This seems unfair - is there any way to avoid it? Lydia, via email.  MSE Kit's A: There's no way to avoid it other than in some exceptional circumstances, eg, if you or your partner dies. Quite simply, an early repayment charge kicks in when you pay off your mortgage before the end of an agreed fixed or tracker period. MSE Kit's A: There's no way to avoid it other than in some exceptional circumstances, eg, if you or your partner dies. Quite simply, an early repayment charge kicks in when you pay off your mortgage before the end of an agreed fixed or tracker period. If you're selling up and using the proceeds to pay off the debt, this counts as paying it off early. Likewise, if you're selling your place to buy a new home with a new mortgage then the new home loan will pay off the debt on the old home loan - also paying it off early. Before you commit to anything, it's best to get advice from a mortgage broker if you're not sure what to do. Eg, if you're getting a new home then you may be able to take your existing mortgage with you - called 'porting'. You won't pay early repayment charges if you do this but it's not right for everyone, hence the need for advice. See Cheap Mortgages for more help. Please suggest a question of the week (we can't reply to individual emails). | RINGING THE CHANGES - WHAT WOULD YOU DO WITH A RED PHONE BOX? That's it for this week, but before we go... BT is putting red phone boxes up for 'adoption', with 1,000s still available. Communities can pay just £1 to refit one and find an entirely new use - some have become art galleries, libraries and even a disco. It's got MoneySavers talking about how they'd transform their local box, with suggestions so far including turning them into a mini greenhouse, public toilet, foodbank and free-to-use jukebox. Read all the ideas and add your own in our How would you transform an old phone box? Facebook thread. We hope you save some money,

The MSE team | |

No comments:

Post a Comment